With IMRF's Reversionary Annuity, you can choose to take a smaller pension when you retire and provide a monthly survivor pension to any person you choose. This person is called your Reversionary Beneficiary.

This Reversionary Annuity is separate from the IMRF surviving spouse pension and the $3,000 lump sum death benefit.

Who can I choose to be the recipient of a Reversionary Annuity?

You can choose any individual you wish to be your Reversionary Beneficiary.

For example, you can choose a Reversionary Annuity to:

- Provide a spouse with retirement income in addition to their IMRF surviving spouse pension

- Provide a spouse who is not eligible for an IMRF surviving spouse pension with retirement income

- Provide any other individual with a lifetime monthly pension, such as a child, an ex-spouse, or any other person. Your Reversionary Beneficiary does not have to be a relative.

How does IMRF reduce your pension if you choose the Reversionary Annuity?

The younger the age of your Reversionary Beneficiary, the greater the reduction in your monthly pension.

For example, if you name a child, the child may receive pension payments for 40, 50, or 60 years. Therefore, the reduction in your pension would be greater than if you name an individual who is closer in age to you.

What choices do you have under the Reversionary Annuity?

Your options depend on whether your spouse is eligible for an IMRF surviving spouse pension.

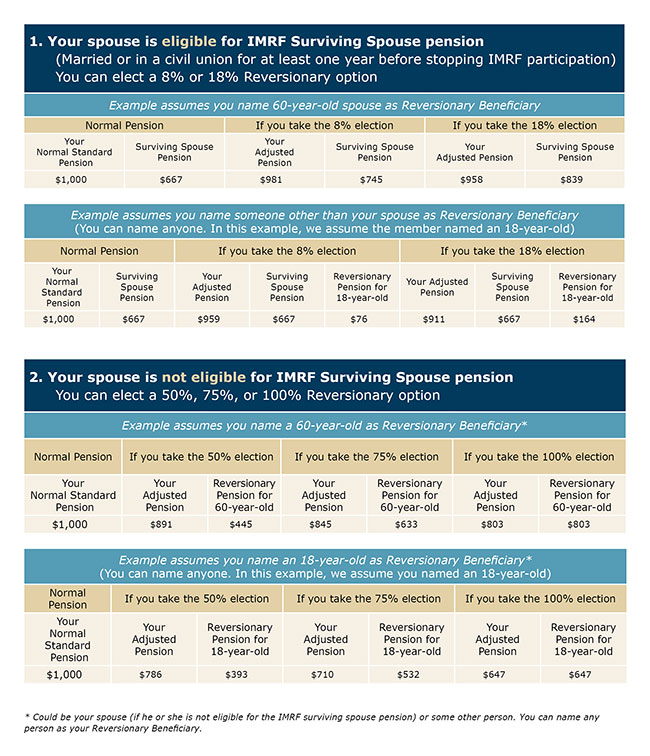

- If your spouse is eligible for a surviving spouse pension:

You can choose a Reversionary Annuity that will provide your spouse—or some other person—an additional pension equal to 8% or 18% of your reduced pension.

Note: Your spouse will still receive a surviving spouse pension equal to 50% of the unreduced pension you would have been receiving had you not chosen a Reversionary Annuity. This is the case whether or not you choose your eligible surviving spouse as your Reversionary Beneficiary. - If you have no spouse or your spouse is not eligible for a surviving spouse pension

You can elect a Reversionary Annuity that will provide your Reversionary Beneficiary with a pension equal to 50%, 75% or 100% of your reduced pension.

Note: In cases where a member's spouse is not eligible for a surviving spouse pension, this option allows the member to provide a benefit similar to IMRF's surviving spouse pension.

Examples of amounts payable under Reversionary Annuity for Tier 2

The examples below are based on the Member retiring at age 65. Amounts vary if retiring at a different age.

Limitations and restrictions of a Reversionary Annuity

- To choose a Reversionary Annuity, submit a "Reversionary Annuity Application" form (Available in Member Access).

At retirement, you will receive an "Preliminary Benefit Statement - Pension" letter that will provide the amounts payable under the various options.

Once you receive your “Preliminary Benefit Statement - Pension" letter, you can:- Select the Reversionary Annuity option you want, or

- Cancel your decision to elect a Reversionary Annuity option

- You can name only one individual to receive this pension. You cannot name a trust or institution.

- You can name any person to receive the Reversionary Annuity (your "Reversionary Beneficiary"); Your Reversionary Beneficiary does not have to be a relative or spouse.

- If you choose to receive a reduced pension, you cannot change the:

- Person who will be your Reversionary Beneficiary

- Amount of the reduced pension you will receive

- If the individual you name (the "Reversionary Beneficiary") dies before you, the pension that would have been paid to him or her is no longer payable. Your pension will not be adjusted.

Once you agree to reduce your pension, the reduction is permanent.

Contact IMRF

Contact IMRF

We want to hear from you whenever you have questions or concerns.