Avoid Violating Working After Retirement Rules

All IMRF employers must comply with rules regarding when a retiree can work for a public sector employer. Audits of employers frequently uncover retiree work violations. Violating these rules can not only harm a retiree's financial security in retirement, but can also cause significant complications for your employer, including:

- Financial: After adjusting wages for each month the retiree should have been enrolled, your employer must pay both employer and member contributions for those months. It is your employer’s responsibility to then recover the member's contributions. Your employer may also have to pay up to half of the total annuity payments the member received when they should not have.

- Lost Efficiency: When a violation is uncovered, your employer must go back and adjust wages for every month that should have been reported. Often the violation covers a span of several years. The time required to correct these errors can be significant.

- Damaged Credibility: Causes of these violations can range from a lack of understanding about the laws governing IMRF to deliberate attempts to overlook the rules. In all cases, these errors damage the reputation of your employer, IMRF, and public pensions in general.

What should you do?

Many different factors determine whether a retiree's pension will be affected by working after retirement, including specific details about his or her work history and pension calculation. To prevent violations:

- Always call IMRF before hiring an IMRF retiree, regardless of the hourly standard of the position the retiree will hold

- Instruct the retiree to contact IMRF to discuss how his or her pension may be affected

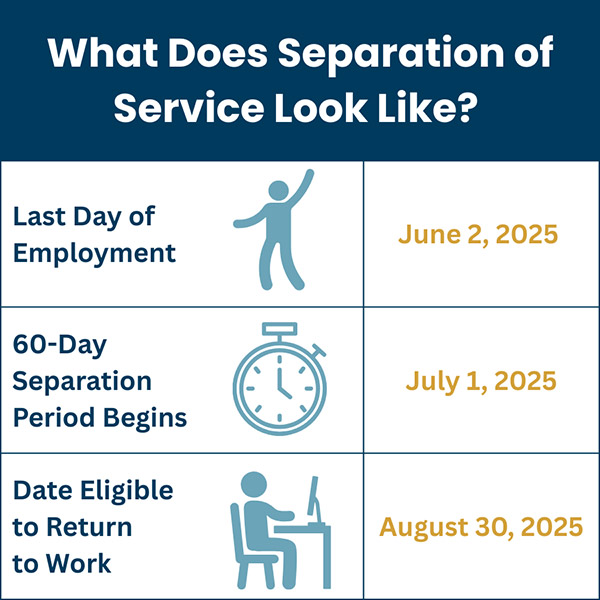

Separation of Service Rules

To comply with the Pension Code and IRS regulations, the IMRF Board has adopted new separation of service rules.

New Rules Effective January 1, 2021

These rules apply to members who terminate participation on or after January 1, 2021:

- To be eligible to start an IMRF pension, at the time of retirement a retiree cannot be working in any capacity for any IMRF employer. This includes temporary or part-time work (regardless of the number of hours worked), volunteering, or working as an independent contractor or leased employee. One exception exists for retirees who are elected or appointed to an elected position, as long as no part of their pension is based on service from that elected office.

- Before the pension start date and within 60 days after, no pre-arrangement (even an informal one) can be made between a retiring member and an IMRF employer that the member will return to work. This includes temporary and part-time work (regardless of the number of hours worked), volunteering, or working as an independent contractor or leased employee. If a pre-arrangement is made prior to or within 60 days after the pension start date, the retiree is not eligible to receive an IMRF pension.

- A new retiree cannot work for any IMRF employer for at least 60 days. After 60 days from the pension start date, a retiree may return to work for an IMRF employer, as long as there was no pre-arranged agreement made before retirement. If a retiree returns to work, the usual return to work rules will apply.

Consequences of Not Separating from Service

IMRF will immediately suspend the pension of any IMRF retiree who performs any type or amount of work for any IMRF employer within 60 days of their pension start date, or who prearranges returning to employment with an IMRF employer after retirement. Retirees who violate this policy must pay back all pension payments that they have received, because they did not truly separate from service.

For More Information

For detailed information about Separation of Service Rules, read General Memo 686 or read the full resolution here.

Overview of Return to Work Rules

Return to work rules are complex, and not all rules are listed on this page. Some of the main points include:

- If a retiree returns to work for an IMRF employer, they must keep track of the hours they work. If they end up working enough hours to reach the employer's hourly standard, you must immediately enroll them in IMRF and their pension must stop, or they must immediately stop working. See the chart below for additional details. (An exception may exist for certain SLEP retirees, call IMRF for details.)

- If a member retired under the IMRF Early Retirement Incentive, he or she can never work for any IMRF employer, even in a position that does not participate in IMRF or as an independent contractor. (An exception may exist for certain elected positions, call IMRF for details.)

- Tier 2 retirees have additional return to work restrictions and should call IMRF before returning to work for any public sector employer in Illinois.

| Rules for Returning to Work | |

|---|---|

If a retiree returns to work for an IMRF employer, they must:

|

|

| If within these 12 months the retiree: |

Then |

| Works below your employer's hourly standard (either 600 or 1,000 hours) | The retiree's pension payments can continue. |

| Is approaching your employer's hourly standard (either 600 or 1,000 hours) but the retiree wants his or her pension to continue | The retiree must:

|

| Reaches or exceeds your employer's hourly standard (either 600 or 1,000 hours) |

|

| Unexpectedly reaches your employer's hourly standard (for example the retiree filled in for another employee and went over without realizing it) but the retiree wants his or her pension to continue | The retiree must

|

Hourly Standards and Returning to Work

If you are hiring an IMRF retiree, you should base the chart above on your employer's hourly standard, with one exception: if your employer changed its hourly standard from 600 to 1,000 hours, any member who participated under your employer before it changed its hourly standard remains grandfathered under 600 hours for your employer.

If your employer changed its hourly standard and you are hiring an IMRF retiree who participated with your employer under a 600-hour standard, he or she will be subject to the 600-hour standard even though your employer is now under the 1,000-hour standard.

An exception may exist for certain SLEP retirees. Call IMRF for details.

Independent Contractors

Some employers think that hiring an IMRF retiree as an independent contractor will avoid any potential consequences to the retiree’s pension. This is not always the case. A retiree’s pension could be affected by working as an independent contractor if:

The retiree retired under the Early Retirement Incentive (ERI)

If an ERI retiree returns to work for any IMRF employer in any position, even as an independent contractor, his or her pension will be affected. Not only will the pension be suspended, but severe financial penalties apply.

The retiree is incorrectly classified as an independent contractor

In this case, even if the retiree did not retire under an ERI, his or her pension could be affected. In addition, if you have incorrectly classified an employee (including non-retirees) as an independent contractor, you are subject to assessment for retroactive IMRF contributions, and you may be held liable for employment taxes for that employee.

The Internal Revenue Service (IRS) has specific requirements for what qualifies as an independent contractor classification and has the authority to make official determinations regarding the classification of an employee. If your employer and IMRF cannot resolve a dispute over a job classification, your employer will be required to seek an official determination regarding the position from the IRS.

For detailed information, see Section 3.60A of the Manual for Authorized Agents, or visit Topic 762 on the IRS website.

Working After Retirement Rules

Working After Retirement Rules

See General Memo 686 and General Memo 688 for more details on the new separation from service rules and the new return to work rules that apply to positions with an IMRF employer.