Impact of 2018 Investment Return on Employer Funding Status, Employer Reserves, and Future Employer Contribution Rates

February 13, 2019

Executive Summary

This preliminary information is based on unaudited investment return data and projected actuarial information. Finalized information will be available in May 2019.

The estimated 2018 investment return for IMRF is (4.31)%. This return translates into investment loss of approximately $1.61 billion, after investment and administrative expenses. Member and annuitant reserves were credited with approximately $2.12 billion, 7.5% interest as required by the Illinois Pension Code. Employer reserve balances were debited, approximately $(4.43) billion. On average, employer accounts were debited approximately (35.59)% of net interest and residual investment loss on their beginning of the year employer reserve balance. This debit reflects the fact that, as a sponsor of a defined benefit plan, IMRF employers share all the risks and rewards of investment returns.

In April and May 2019, IMRF will present a series of local Employer Rate Meetings throughout the state. At these meetings, the impact of year-end financial and actuarial data on IMRF as a whole and its estimated impact on individual employers will be discussed. Current topics impacting IMRF and pension plans in general will also be discussed. IMRF will present the same information during an online webinar in May 2019.

Investment Returns

IMRF’s investment returns reflect financial markets over a calendar year. IMRF reports both a market basis return and an actuarial return. IMRF’s estimated 2018 investment return on a market basis is (4.31)%. IMRF’s estimated actuarial return is (5.41)%, due to five-year smoothing (see graph). The actuarial return is used to determine employer contribution rates and actuarial funding status. The actuarial return moderates fluctuation in employer contribution rates, and smooths the recognition of market returns that either exceeds or falls short of the assumed actuarial return of 7.5%, as of December 31, 2018.

Employer Funding Status

In April 2019, IMRF will furnish each employer its annual GASB 50 information as well as GASB 68 footnote information for 2018. This information will disclose both the actuarial and market-based funding status for all plans for their active and inactive members. Annuitant information is included in the GASB 68 report.

Important Note: the assumed rate of return (ARR) was decreased by one quarter percent to 7.25% as of January 1, 2019. This change was made in recognition of the overall decline in market returns and is consistent with market return assumptions made by pension plans across the country.

Given the decline in IMRF’s assumed rate of return and the negative market returns in 2018, employers should expect the funding status of their plan to decrease on both an actuarial and market-value basis and, consequently, 2020 employer contribution rates will more than likely increase.

Impact on Employer Reserves

By statute, IMRF must credit member and annuitant reserves with 7.50% interest annually on their opening reserve balance amounts (approximately $2.12 billion for 2018).

At the same time, IMRF must charge (debit) this same amount back to employers’ reserve balances, along with other costs, gains or losses:

| Member and Retiree Reserves | $(2.12b) |

| Administrative/Investment Expenses | (0.17b) |

| ARR Adjustment | (0.53b) |

| Investment Loss | (1.60b) |

| Total Charge/Debit to Employers | $(4.43b) |

|---|

On average, employers will be debited approximately 35.59% based on their beginning-of-the-year employer reserve balance. This debit reflects the fact that, as a sponsor of a defined benefit plan, IMRF employers share all the risks and rewards of investment returns. The actual amount debited to individual employers will vary from the average due to differences in employer and annuitant reserve amounts.

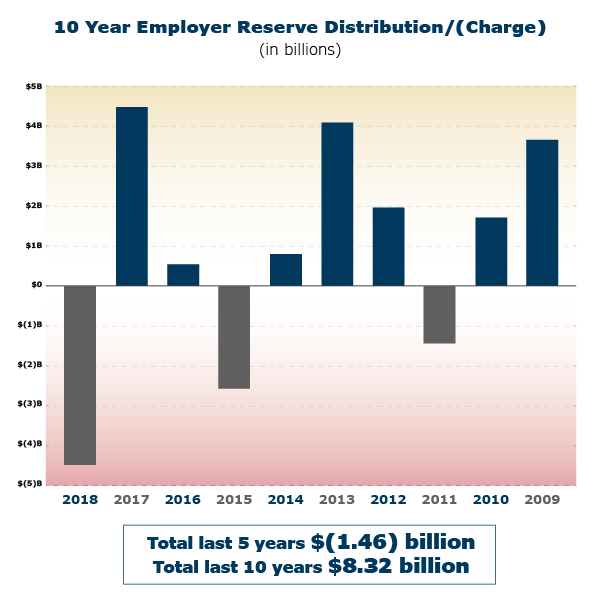

Over the last 10 years, IMRF employers have been credited or (charged) the following amounts:

Employer Contribution Rates

Employer contribution rates consist of as many as six parts:

- Normal retirement costs

- Death in service benefits

- Temporary disability benefits

- Supplemental retirement benefits (the 13th payment)

- Amortization of over- or underfunding

- Early Retirement Incentives (employer option)

The ongoing cost of the IMRF benefit package for the regular plan covering normal retirement costs, death in service benefits, temporary disability benefits, and supplemental retirement benefits was 7.61% of payroll in 2018. Put another way, for each dollar of service an employee renders, the employer also incurs a pension cost of 7.61 cents. If an employer is overfunded, the 7.61 cents is reduced and IMRF draws from the surplus. If an employer is underfunded, the 7.61 cents is increased to collect the shortfall.

Average employer rates over the past five years:

| Year | Rate |

|---|---|

| 2019 | 9.06% |

| 2018 | 11.24% |

| 2017 | 11.34% |

| 2016 | 11.73% |

| 2015 | 11.69% |

Individual employer contribution rates vary from the average since each employer has a unique rate affected by its own demographics and funding status as well as a unique mix of Tier 1 and Tier 2 members. Employer rates will be impacted by the lowered the assumed rate of return to 7.25% as of January 1, 2019.

IMRF Meetings

To discuss the potential impact on individual employers in 2019, 2020 and beyond, IMRF will conduct a series of Employer Rate Meetings throughout the state in April and May 2019. Current topics impacting IMRF and pension plans in general will also be discussed. In May, IMRF will present a webinar that will also discuss this information.

Additional details and registration information for the Employer Rate Meetings and the webinar will be available on IMRF’s website, www.imrf.org, and in upcoming editions of Employer Digest e-newsletter.

Questions

If you have any questions regarding the information presented in this General Memo, please call or email Mark Nannini, Chief Financial Officer, at (630) 368-5345 or mnannini@imrf.org.