IMRF investment returns are the largest driver of changes in employer contribution rates from year to year. IMRF assumes its investment portfolio will earn 7.25% over the long-term. When IMRF exceeds that return assumption, employer contribution rates go down in future years. When IMRF falls below that return assumption, employer contribution rates go up in future years.

Because investment returns vary widely each year, IMRF uses an industry-standard best practice called “smoothing” to limit employer rate volatility. As is common in the pension industry, each year IMRF only recognizes 20%—or 1/5th—of its investment gain or loss for employer rate-setting purposes. So, for rate-setting purposes, it takes five years for IMRF to fully recognize the investment gains or losses from any one year.

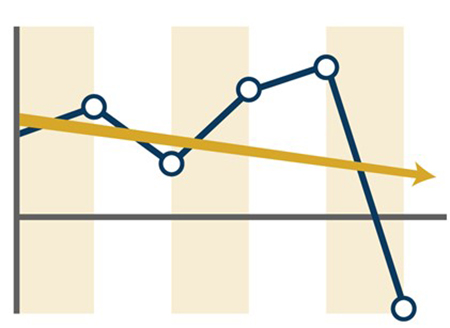

Rate impact from investment results smoothed over a five-year period

Figure one: The yellow line represents an example of the impact of

IMRF’s annual investment results on employer contributions.

IMRF’s annual investment results on employer contributions.

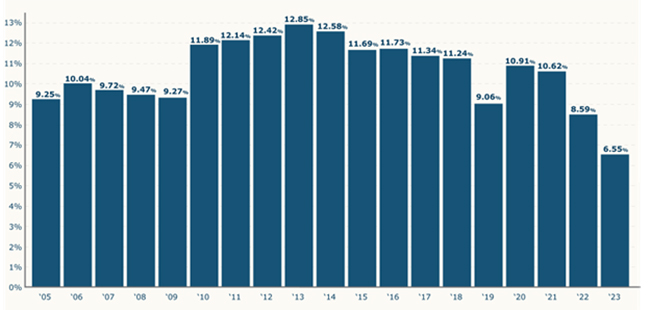

This practice keeps annual employer rates stable despite investment return’s inherently volatile nature. The average Regular Plan employer contribution rate in 2023 is 6.55% of payroll. Twenty years ago, in 2003, the average Regular Plan employer contribution rate was 6.22%.

History of returns 2005 to present

The effect of IMRF’s investment results on future employer contributions

IMRF will release its estimated 2022 investment return early next month. Like most investors, the IMRF investment portfolio decreased in value during 2022. There is a two-year lag before investment results first affect employer rates, so the 2022 loss will first impact your 2024 employer contribution rates. The amount each employer’s rate will increase in 2024 will vary based on other factors that are unique to each employer. But, in general, smoothing will help mitigate the impact in any one year.

In addition, because of historically high investment returns in recent years and IMRF’s smoothing practices, at the end of 2021 there remained about $7 billion worth of unrecognized investment gains for rate-setting purposes. This is good news for employers because these unrecognized investment gains will reduce some of the rate impact of the 2022 investment loss.

Your employer will receive its 2024 Preliminary Rate Notice in Employer Access in April. To learn more about smoothing and IMRF’s rate-making process, be sure to register for one of the 2023 Rate Meeting Webinars in May. You can watch a recording of the 2022 webinar here.

Download Presentation

Download Presentation

Click here to download the 2022 Employer Rate Webinar Presentation. The animations built into this presentation will only function if you view the PowerPoint in “slide show” mode.

Employer Rates

Employer Rates

Watch the 2022 Employer Rate Webinar video presented by IMRF Executive Director Brian Collins and Chief Financial Officer Mark Nannini.