You contribute 4.5% of your salary toward your future IMRF pension:

- 3.75% for a regular plan benefit

- 0.75% for a surviving spouse pension

If you do not have an eligible surviving spouse when you retire, you can take your surviving spouse contributions as a lump sum refund or you can convert them into a separate lifelong pension payment.

Under Tier 2, a member's wages are capped at $129,192.26 in 2026. You do not pay any contributions on wages above the cap. Even though wages aren't reported, you will continue to earn service credit.

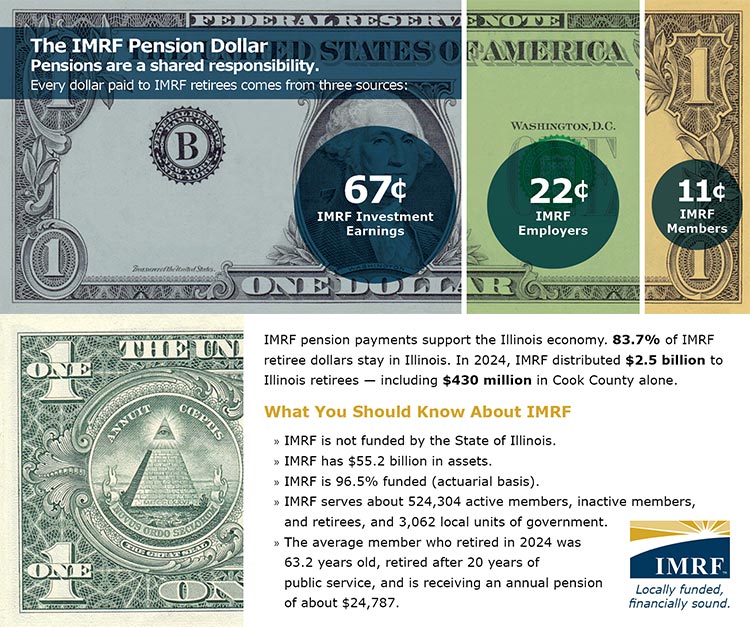

What You Get By Contributing to IMRF

Once you are eligible for an IMRF pension you are guaranteed your pension for life. When you start receiving your IMRF pension, you will likely receive the total amount of your contributions back within the first few years of your retirement. The remaining lifelong pension payments you receive will be paid by your employer's contributions and investment earnings. This is why your IMRF pension is such a valuable benefit.

IMRF also provides important disability and death benefits.

You Never Lose Your Contributions

You are guaranteed a return of your IMRF contributions, paid as either:

- Your IMRF pension

- A refund

- Death benefits

Participation in IMRF is Required

If you are working in a position that qualifies for IMRF you must contribute -- IMRF is not an optional program. (There are exceptions for city hospital workers and elected officials.)

You Cannot Borrow from Your IMRF Contributions

You cannot borrow from your contributions or use them as collateral for a loan. As long as your contributions are on deposit with IMRF, they cannot be garnished or seized by any creditor.

Contributions are Tax-Deferred

You do not pay federal or Illinois income tax on the money used to make your contributions.

Reaching Maximum IMRF Pension Benefit

IMRF Regular plan members receive the maximum pension after earning 40 years of Regular service credit. If you have 40 or more years of service credit, you can elect to stop making IMRF contributions. If you stop contributing, you will still have the same disability and death benefit protection as contributing members.

Please request a pension estimate before you elect to stop making contributions. If your salary is still increasing it may not be in your best interest to stop your contributions. Once you return a completed "40-Year Service Election to Cease Contributions" form (Available in Member Access), you cannot change your mind.

Did you know?

Did you know?

You cannot borrow from your contributions or use them as collateral for a loan. As long as your contributions are on deposit with IMRF, they cannot be garnished or seized by any creditor.

Tier 2 members do not pay any contributions above the wage cap. The wage cap for 2026 is $129,192.26.

{kind=link}